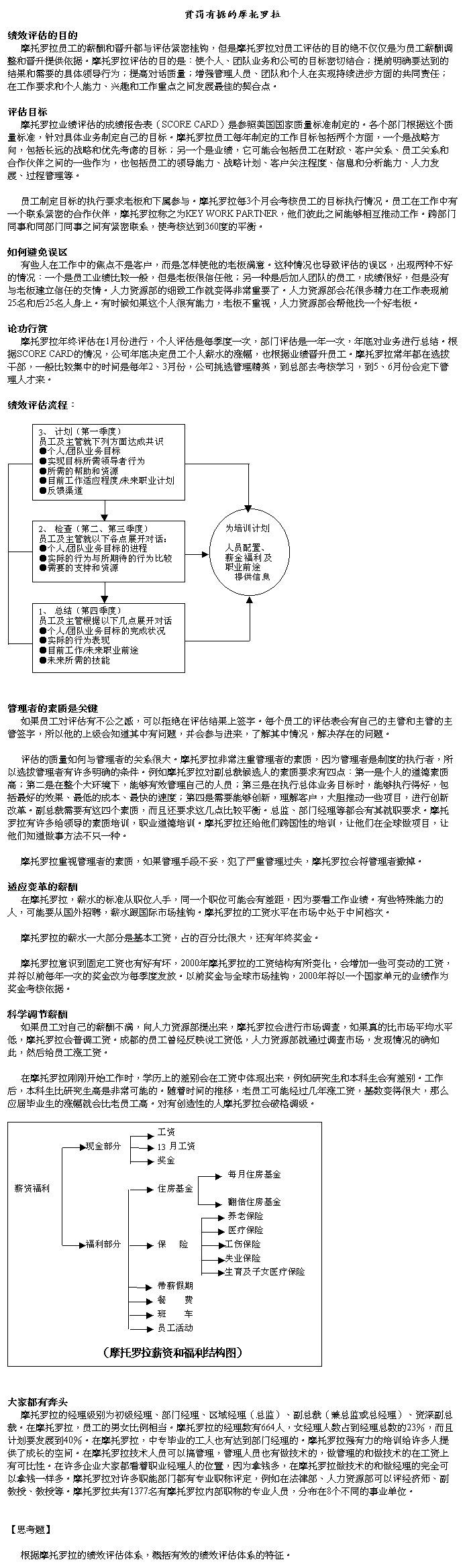

北大MBA分析案例库

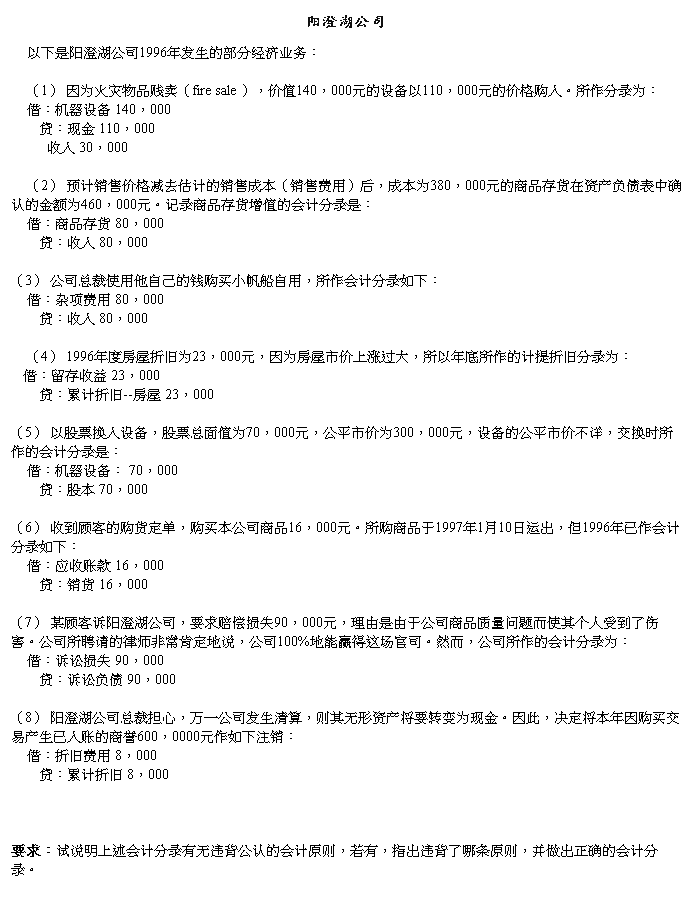

第二篇:MBA资源-北大MBA原文案例库

MBA资源

欢迎下载

各种资料大全!!!

精品水晶,动人礼品

我的网店 :

欢迎下载

各种资料大全!!!

我的网店 :

How Financial Firms Decide on Technology,介绍国际大银行在决定对信息技术投资时的考虑要点和

他们具体的实施过程。

How Financial Firms Decide on Technology

(Abstract)

The financial services industry is the major investor in information technology(IT) in the U.S. economy; the typical bank spends as much as 15% of non-intereste expenses on IT. A persistent

finding of research into the performance of financial institutions is that performance and efficiency vary widely across institutions. Nowhere is this variability more visible than in the outcomes of the IT investment decisions in these institutions. This paper presents the results of an empirical investigation of IT investment decision processes in the banking industry. The purpose of this investigation is to uncover what, if anything, can be learned from the IT investment practices of banks that would help in understanding the cause of this variability in performance along with pointing toward management practices that lead to better investment decisions. Using

PC banking and the development of corporate Internet sites as the case studies for this

investigation, the paper reports on detailed field-based surveys of investment practices in several

leading institutions

How Financial Firms Decide on Technology

(Part One)

信息技术对金融服务业的影响正在增加,不仅仅表现在银行的15%无息开支上,而且对金融服务业的运做和战略也有很强的影响。

一个对金融机构的长期研究表明,不同的机构的效率和表现也不同。其决定的因素有以下一些其中的一个因素就是对投资的决定和管理。SBS是一个失败的例子,但是成功的公司也不少。本文注重解答以下的问题:

1.银行对IT投资的评估和管理过程?

MBA资源

MBA资源

2.在对IT的管理过程中,理论和实际操作的结合如何?

3.IT投资的管理和银行性能的关系如何?

1.0 Introduction

Information technology(IT) is increasingly critical to the operations of financial services firms. Today banks spend as much as 15% of non-interest expense on information technology. It is estimated that the industry will spend at least $21.1

billion on IT in 1998, and financial institutions collectively account for the majority of IT investment in the U.S. economy. In additon to being a large component of the cost structure, information technology has a strong influence on financial firms operatons and strategy. Few financial products and services exist that do not utilize computers at some point in the delivery process, and a firms'information systems place strong

constraints on the type of products offered, the degree of customization possible and the speed at which firms can respond to competitive opportunities or threats.

A persistent finding of research into the performance of financial institutions is that performance and efficiency varies widely across institutions, even after

controlling for factors such as size(scale), product breadth(scope), branching behavior and organizational form(e.g. stock versus mutual for insurers; banks versus saving & loans). Given the central role that technology plays in these institutions, at least some of this variation is likely to be due to variations in the use and effectiveness of IT investments. While some authors have argued that the value of IT investment has been insignificant, particularly in services, recent empirical work has suggested that IT investment, on average, is a productive investment. Perhaps more importantly, there appears to be substantial variation across firms; some firms have very high

investments but are poor performers, while otheres invest less but appear to be much more successful. Brynjolfsson and Hitt found that as much as half the returns to IT investment are due to firm specific factors.

One potentially important driver of differences in IT value, and of firm

performance more broadly, is likely to be the decision and management peocessed for IT investments. Horror stories of bad IT investment decisions abound. Consider the example of the new strategic banking system(SBS) at Banc One(American Banker 1997). Banc One Corp. and Electronic Data Systems Corp. agreed last year to end MBA资源

MBA资源

their joint development of this retail banking system after spending an estimated $175 million on it. As stated in the American Banker article, SBS"was just so

overwhelming and so complete that by the time they were getting to market, it was going to take too long to install the whole thing," said Alan Riegler, principal in Ernst & Young's financial services management consulting division. However, not all the stories are negative. New IT systems are playing a vital role in reshaping the delivery of financial services. For example, new computer-telephony integration(CTI) technologies are transforming call center operations in financial institutions. By investing in technology, more and more institutions are moving operations from

high-cost branch operations to the telephone channel,where the cost per transaction is one-tenth the cost of a teller interaction. This IT investment not only reduces the cost of serving existing customers, but also extends the reach of the institution beyond its traditional geographic boundaries.

In this paper, we utilize detailed case studies of six retail banks to investigate several interrelated questions:

1.What processes do banks utilize to evaluate and manage IT investments?

2.How well do actual practices align with theoretical arguments about how IT investments

should

be managed?

3.What impact does that management of IT investments have on performance?

How Financial Firms Decide on Technology

(Part Two)

For the first question, we develop a structured framework for cataloging IT investment practices and then populate this framework using a combination of surveys and semi-structured interviews. We then compare the results of this exercise with a synthesis of the literature on IT decision

making to understanding how practices vary across firms and the extent to which this is consistent with "best practices" as described in previous literature. Finally, we will compare these processes to internal and external performance metrics to better understand which sets of practices appear to be most effective.

To make these comparisons concrete, we examine both the general decision process as well as the specific processes used for two recent IT investment decisions :the adoption of

computer-based home banking (PC banking), and the development of the corporate web site. MBA资源

MBA资源

These decisions were chosen because they were recent and are related but provide some contrast; in particular, PC banking is a fairly well defined product innovation, while the corporate web presence is more of an infrastructure investment which is less well-defined in terms of objectives and business ownership.

Overall, we find that while some aspects of the decision process are fairly similar across

institutions and often conform to "best practice" as defined by previous literature, there are several areas where there is large variation in practice among the banks and between actual and theoretical best practice. Most banks have a strong and standardized project management for ongoing systems projects, and formal structures for insuring that line-managers and systems people are in contact at the initiation of technology projects. At the same time, many banks have relatively weak

processes(both formal and informal) for identifying new IT investment opportunities, allocating resources across organizational lines, and funding exploratory or infrastructure projects with long term or uncertain payoffs.

The reminder of this paper is organized as follows. Section 2 describes the previous literature on performance of financial institutions and the effects of IT on performance. Section 3 describes the methods and data. Section 4 describes the current academic thinking on various components of the decision process and compares that to actual practices at the banks we visited. Section 5 describes the results of our in-depth study of PC banking projects and the summary, Section 6 contains a similar analysis for the Corporate Web Site and discussion and conclusion appear in Section 7.

How Financial Firms Decide on Technology

(Part Three)

2.0 Previous Literature

2.1 Performance of Financial Institutions

There have been a number of studies that have examined the efficiency of the banking industry andthe role of various factors such as corporate control structure (type of board, directors, insider stock holdings, etc.), economies of scale (size), economies of scope (product breadth), and branching strategy; see Berger, Kashyup and Scalise (1995) and Harker and Zenios (forthcoming) for a review of the banking efficiency literature. While there is substantial debate as to the role of these various factors, there is one unambiguous result: that most of the (in) efficiency MBA资源

MBA资源

of banks is not explained by the factors that have been considered in prior work. For example, Berger and Mester (1997) estimate that as much as 65-90% of the x-inefficiency remains

unexplained after controlling for known drivers of performance. A similar story also appears in insurance where "x-efficiency" varies substantially across firms when size, scope, product mix, distribution strategy and other strategic variables are considered. It has been argued that one must get "inside the black box" of the bank ot consider the role of organizational, strategic and technological factors that may be missed in studies that rely heavily on public financial data.

2.2 Information Technology and Business Value

Early studies of the relationship between IT and productivity or other measures of

performance were generally unable to determine the value of IT conclusively. Loveman (1994) and Strassmann (1990) ,using different data and analytical methods both found that the

performance effects of computers were not statistically significant. Barus, Kriebel and

Mukadopadhyay (1995), using the same data as Loveman, found evidence that IT improved some internal performance metrics such as inventory trunover, but could not tie these benefits to

improvements in bottom line productivity. Although these studies had a number of disadvantages (small samples, noisy data ) which yielded imprecise measures of IT effects, this lack of evidence combined with equally equivocal macroeconomic ananlyses by Steven Roach (1987) implicitly formed the basis for the "productivity paradox". As Robert Solow (1987) once remarked, "you can see teh computer age everywhere except in the productivity statistics."

More recent work has found that IT investment is a substantial contributor to firm

productivity, productivity growth and stock market valuation in a sample that contains a wide range of industries. Brynjolfsson and Hitt (1994,1996) and Lichtenberg (1995) found that IT investment had a positive and statistically significant contribution to firm output . Brynjolfsson and Yang (1997) found that the market valuation of IT capital was several times that of ordinary capital. Brynjolfsson and Hitt also found a strong relationship between IT and productivity growth and taht this relationship grows stronger as longer time periods are considered. Collectively ,these studies suggest that there is no productivity paradox, at least when the analysis is performed across industries using firm-level data. The differences between these results and earlier studies is probably due to the use of data taht was recent , more comprehensice ,and more disaggregated (firm level rather than industry or economy level).

Most previous sutdies have considered the effects of technology across firms in multiple industries, although a few studies have considered the role of technology in specifically in the banking industry. Steiner and Teixiera surveyed the banking industry and argued that while large MBA资源

MBA资源

investments in technology clearly had value,little of this value was being captured by the banks themselves; most of the benefits were being passed on to customers as a result of intense competition. Alpar and Kim examined the cost efficiency of banks overall and found that IT investment was associatied with greater cost efficiency although the effects were less evident when financial ratios were used as the outcome measure. Prasad and Harkere examined the relationship between technology investment and performance for 47 retail banks and found positive benefits of investments in IT staff.

While these studies show a strong positive contribution of IT investment on average, they do not consider how this contribution (or level of investment )varies across firms. Brynjolfsson and Hitt found that "firm effects" can account for as much as half the contribution of IT found in these earlier studies. Recent results suggest that at least part of these differences can be explained by differences in organizational and strategic factors. Brynjolfsson and Hitt found that firms that use greater overall IT benefits. Bresnehan, Brynjolfsson and Hitt found a similar result for firms that have greater levels of skills and those that make greater investments in training and

pre-employment screening for human capital . In addition, strategic factors also appear to affect the value of IT. Firms that invest in IT to create customer value (e.g. improve service, timeliness, convenience, variety) have greater performance than firms that invest in IT to reduce costs. While these studies are begining to explore how the performance of IT investment varies across firm, particularly due to organizational and strategic factors, little attention has been paid to the technology decision making process.

How Financial Firms Decide on Technology

(Part Four)

2.3 IT Investment Decisions

While there is no concise definition of "best practice" in IT investment decisions, there are a number of consistent arguments advanced in the IT management literature that can be synthesized into an understanding of the conventional wisdom.

For the pruposes of discussion it is useful to subdivide the process of IT management into seven discrete, but interrelated processes. The first six processes are oriented around the proposal, development and management of IT projects, while the last process is about maintaining the capabilities of the IT function and its interrelationships with the rest of the business:

1.Identification of IT opportunities

2.Evaluating opportunities

MBA资源

MBA资源

3.Approving IT projects

4.The make-buy decision

5.Managing IT projects

6.Evaluating IT projects

7.Manage and Develop the IT Function

This subdivision loosely corresponds to many of the major issues in IT management such as outsourcing, line management-IT alignment, software project management, and evaluating IT investments.

In addition, this list loosely corresponds to frameworks for the management of IT. The primary difference is that this list views the IT management process as managing a stream of projects rather than focusing on the function of the IT department overall or the role of the CIO, the typical perspective in the previous literature. For example, a common framework used to align IT to business starategy, the critical success factors(CSF) method, include three workshops: the first to identify and focus objectives, the second to decide and prioritize on systems investment, and the third to develop, deploy and reevaluate prototype systems. Boynton, Jacobs and

Zmud(1992) identify five critical IT management processes: setting strategic direction,

establishing infrastructure systems, scanning technology, transferring technology and developing systems. Rockart, Earl and Ross(1996) propose eight imperatives for the IT organization which can be grouped into managing the IT-business relationship, building and managing systems and infrastructure, managing vendors, and creating a high performance IT organization. Thus, while previous work has subdivided the process in different ways, collectively the studies cover all the seven processes we examine.

We will discuss each of the individual points in detail below.

2.3.1 Identificant of Opportunities

Historically, the IT function was primarily reactive, responding to requests by business units.

A business unit. A business unit manager would identify a need for a new system or a

repair/enhancement to an existing system and communicate this need to the IT function. The IT personnel would then evaluate the idea for technical feasibility and develop a project proposal include an initial determination of resource needs, cost, and delivery time. While this makes effective use of IT personnel in evaluating particular ideas, it provides only a limited role for IT personnel to aid in the identification of technology-based business opportunities.

For that reason, some authors have suggested that the IT function should play a larger role in the identification of technological opportunities. For example, Davenport and Short (1990) MBA资源

MBA资源

emphasize that IT capabilities should inform business needs as well as the business units placing demandson the IT function. Fockart, Earl and Ross and Boynton, Jacobs and Zmud identify the role of "technology scanning" and "technology education" as an important component of a

centralized IT department; they argue that information systems specialists should be reponsible for evalusting new technologies for business applicability since business units will generally lack the resources or the technological capability to perform these evaluations themselves. Moreover, central IT is best positioned to educate the end uses to make them good "custmers" of the central IT group.

In the banking industry, IT may be able to play an additional role in coordinating technology. Because banks and other financial firms are often managed with largely autonomous business units (for example, banks are often divided into product lines ---cash management,

investment----or along customer segments---wholesale, commercial, retail) only the central IT function will have a perspective over the porfolio of systems projects and capabilities. One critical role in this respect is the provision and development of the shared IT infrastructure (e.g. central processors, networks, software standards, etc.). Often these projects naturally span business units such that the only ral owner is the IT function; also they generally tend to be highly technical and thus the natural responsibility would also fall on the IT department.

How Financial Firms Decide on Technology

(Part Five)

2.3.2 Evaluating Oppoutunities

Once a project is at least initially defined, there is a process by which the initial idea is converted into a proposal that can be evaluated by management for approval or rejection of funding.

In the last ten years, it has become more or less standard practices to develop a business case or business plan for any substantial IT investment (some small maintenance projects are simply done on request), although the content, sophistication and formality of this process varied

substantially. The most typical of these project proposals (assuming a mid-size to large project) take the form of a business plan which includes a qualitiative description of the objectives,

competitive environment, a description of the opportunity and, in some cases, an implementation plan. While the form of these plans varies widely, there are some general points of comparison. For the qualitative portion, the major issue is whether the plan explicitly addresses changes in the business environment, or is primarily inward focused. For minor systems enhancement MBA资源

MBA资源

projects with no strategic objective (or even major investments that are not strategic such as year 2000 repairs), it makes sense for the plan to focus entirely on internal issues. However, to the extent that the investment is made for competitive reasons or is likely to spur a reaction from

competitors, it is important to qualitatively evaluate whether the business environment will remain static and , if not, examine possible scenarios that are likely to occur. The assumption of a static business environment is a common decision bias that can particularly plague strategic IT

investments; Clemens (1991) terms this the "trap of the vanishing status quo".

For the quantative financial evaluation, most IT evaluation methods have their roots in traditional capital budgeting procedures such as discounted cash flow analysis(DCF). However, while these techniques can work well for projects where costs and benefits ar well defined (e.g. purchasing off-the -shelf software in pursuit of operational cost savings), it is increasingly

recognized that simple application of DCF approaches is not sufficient for IT investments. This is because much of the value of modern IT investments is likely to be difficult to quantify --such as revenue enhancements or cost savings through improved customer service, product variety, or timeliness. One commonly used stategy is to value non-quantifiable benefits at zero, although this strategy will systematically bias project evaluations to unnecessarily reject projects.

Recognizing the limitation of the DCF approach, several alternative approaches have been proposed. One method is to base tghe case entirely on qualitative analysis; unfortunately, this approach often leads to hightly subjective judgements and is likely to err on the side of accepting bad projects. Kaplan, recognizing this problem in the context of evaluating computer integrated manufacturing (CIM), proposed using a variant of DCF; a firm calculates the present value of the investment using all the components that can be quantified and then compares this prliminary

value to the qualitative list of other benefits and costs. In other cases, where the evaluation is make difficult because of future uncertainties (e.g. market growth and acceptance; response of

competitors ) decision trees or other types of probability based assessment tools may simplify

investment decisios. Finally, for some types of investments or decisions (for example, the decision whether to invest immediately or defer), advanced techniques such as real options can be applied. Although this discussion has focused primarily on evaluating the benefit part of the

quantitative evaluation, there are other difficulties in estimating the cost of IT projects,

particualarly those involving software development. Existing models such as COCOMO of function points estimation are known to improve the ability to predict project length, staffing

requirements and total costs, although they are k own to be systmeatically off by as much as 400%. However, the accuracy of these estimates can also be improved later in the project when

specifications are well defined or by customizing the models to the experience of a particular MBA资源

MBA资源

organization. However, despite the fact that these tools and approaches are readily available many firms still utilize "seat of the pants" estimants or lock in schedules and cost estimants before the projects are fully defined.

How Financial Firms Decide on Technology

(Part Six)

2.3.3 Approving IT Projects

Once a project has been evaluated and a formal project proposal exists, there are a variety of mechanisms that are used to determine which projects should be funded. Most institutions have some form of committee structure, similar to capital budgeting committees, which is responsible for evaluating, modifying and approving projects.

Most of the previous literature on the management of IT has focused on the so-called "IT steering committee" which is an executive level group, often comprised of the heads of business units or their direct reports. The objective of this committee is to ensure that IT strategy is aligned with business unit strategy, projects are coordinated across business units where there are possible synergies and to educate the business unit managers on the both the actual activities of the IT group and the potential IT opportunities.

2.3.4 Make-Buy Decisions(Outsourcing)

At the inception of any project, a firm has the choice of whether to utilize their internal resources in the IT department (insource) or utilize an outside vendor for any or all of a

project(outsourcing). While the market for outsourced services has existed since sale of the first corporate computers, the size of the outsourcing market has grown dramatically in recent years and is expected to grow substantially. In 1997 the market for information technology

outsourcing has been estimated at $26.5 billion in the U.S. and at $90 billion worldwide. Growth estimates of this market range from 15% to 25%.

In general , an outside firm may be advantaged in providing a service previously produced internally, because of economies of scale, scope or specialization. By aggregating demands for multiple clients, vendors can smooth variations in demand increasing capacity utilization and reducing risk, make investments that trade larger fixed costs for lower variable costs, and have MBA资源

MBA资源

stronger incentives to invest in cost-reducing technology. By narrowly focusing on technology, they may be better able to attract, hire , manage and retain high quality personnel due to better ability to tailor management practices, career paths and incentive structures to a specific activity. The value of these benefis is tempered by explicit and implicit costs of using the market or some intermediate form of governance rather than vertical integration. These problems manifest themselves in three types of risk: shirking(under-performance in hard-to-measure tasks),

poaching (misappropriaiton of shared resources ) and opportunistic re-negotiation (exploitation of bargaining disadvantages in ongoing relationships) . Some authors have argued that in IT these risks are so severe that outsourcing has, overall, a poor value proposition. However , there are a number of very successful agreements and the growth in the market over the long term suggests that some economic benefits of outsourcing are present.

In pratice, outsourcing can take many forms and the complexity of these arrangements is increasing. The simplest arrangement is the use of contract workers; the worker is not employed by the firm, but is managed more or less as if they were an employee. This pratice is so common in IT that the presence of contract employees is assumed to be a standard feature of IT

departments. At the next level is selective outsourcing in which a firm outsources particular projects or parts of projects to an outside vendor. This is also quite common in software

development and technical support activities, although any well-defined task could presumably be outsourced in this way. Finally, the firm may choose to outsource the entire IT function, a practice that began in the late 1980s and has continued today.

Hitt, Lorin M., Frei, Frances X. and Patrick T. Harker. (1999) "How

Financial Firms Decide on Technology," in Brookings/Wharton Papers

on Financial Services:1999, Litan, Robert E. and Anthony M. Santomero,

Eds. Washington, DC: Brookings Institution Press.

MBA资源