本科毕业设计(论文)开题报告

题目:我国商业银行的资产负债管理研究

√ 课 题 类 型: 设计□ 实验研究□ 论文□

学 生 姓 名: 尹娟娟

学 号: 3080501201

专 业 班 级: 工商管理082班

学 院: 管理工程学院

指 导 教 师: 贾育青

开 题 时 间: 20xx年4月10日

2012 年 4 月 10 日

1

一、毕业设计(论文)内容及研究意义(价值)

1、毕业设计(论文)内容

经济全球化导致现代商业银行经营环境发生了根本性的变化,对商业银行经营管理提出了新的要求。商业银行资产负债管理研究己成为理论的热点和前沿领域。一方面,我国商业银行的利润来源严重依赖存贷利差。另一方面,我国银行业仍属于局部垄断的行业,市场准入和退出机制不健全。在利率管制放松和行业竞争加剧的条件下,如何从资产负债管理的角度,提升我国商业银行的核心竞争力,防范和化解利率波动风险,对于维护我国金融体系的稳定和缩短我国商业银行与国外同行的差距,加快我国商业银行的发展具有重要的意义。

本人利用业余时间查阅了大量相关的期刊、报纸、著作以及互联网上的文献资料并进行了系统全面的分析和研究。从国内外对资产负债管理的理论发展情况出发,主要研究的是我国商业银行资产负债管理的现状和特点以及出现的问题,对资产负债管理提出浅见,包括完善商业银行内部资产负债管理组织体系,在资本规划的基础上加强风险资产管理,希望提高利率风险管理能力,强化流动性管理、合理配置资金资源。

2. 研究意义(价值)

资产负债作为商业银行经营业务的主要组成部分,直接影响商业银行的经济效益和长远发展,对其进行有效管理具有重要的现实性意义:

(1)避免或减少各种可能的损失

通过采用多元化资产管理和多样化的授信对象,使银行远离由于一家公司或一种行业经营环境恶化而带来的巨额亏损;使各种资产和负债的结构、期限等方面相对称,规避银行利率变化所导致的损失;甚至银行还可以将贷款证券化,将信用风险进行转移,使银行的信用风险降低,保证资产安全。

(2)提高现金流量的稳定性和资金的使用效率

将商业银行的资产和负债结构进行优化,合理的组合,能提高资金的使用效率,使银行资产处理安全状态,规避风险。比如,在商业银行的资产组合中,可以持有一定量的同业贷款、现金、短期证券等,这样可以防止因存款准备金不足而陷入流动性危机,同时又可以避免大量资金闲置,导致资金利用率低下;通过持有期货和期权等保值资产,使银行的汇率风险和利率风险降低,稳定收入和支出。这样,通过各种方法优化资产和负债结构,将现金流量的波动控制在合理的范围以保证正常的资金周转和较高的资金运用效率。

(3)规避和减少风险

2

因事先设置一系列风险指针,制订了完备的风险防范措施,使得银行能监控各种风险,当市场风险或其他风险发生并导致实际损失时,能及时采取有效的措施,避免危机进一步扩散,从而保证银行经营的稳定性和安全性。

(4)提高预测未来收入的能力

比如,商业银行在资产负债管理中,引入资本充足率、利率差已经贷存比率等手段起到控制风险资产规模的作用,这样可以减少收入的不确定性,以达到增强预测未来收入的能力,同时通过持有具有稳定收益的期货和期权,银行可以保证收入的稳定性,增加收入的确定性。

(5)树立良好的企业形象,增强竞争力

对外资银行开放人民币业务以及国内银行的改制,银行业的竞争更加激烈。一间符合监管机构要求、信用良好,并能有效预防和应对金融风险的高品质商业银行,在提供金融产品和服务方面必然更具竞争力,在银行业激烈的竞争中必将处于优势,同时也更容易获得客户的认同,获得稳定持久的客户群体,促进业务快速发展,在竞争中胜出。

二、毕业设计(论文)研究现状和发展趋势(文献综述)

(一)研究现状

针对商业银行的资产负债管理情况,国内和国外的学者们都做过相关研究。

1、国内研究现状

我国商业银行资产负债管理起步较晚。19xx年以前,我国一直实行计划经济下的信贷资金体制,银行的资金由国家分配。19xx年起,商业银行的信贷资金管理实行实贷实存管理体制,将资金与规模分开,实行信贷规模和资金双向控制的管理体制。1987—19xx年实行资产负债比例管理。19xx年2月15日,中国人民银行制定、下发了《关于对商业银行实行资产负债比例管理的通知》,对资本和资产风险权数作出暂行规定,根据国际一般惯例和我国实际情况,规定了9项指标,标志着资产负债比例管理在我国商业银行的全面实施。19xx年12月,中国人民银行又公布了《关于印发商业银行资产负债比例管理监控、监测指标和考核办法的通知》,该通知对94年通知的资产负债比例指标进行修订,主要补充了境外资金运用比例、国际商业借款指标,增加了六项监测性指标,并把外汇业务、表外业务纳入考核体系。19xx年1月1日起,取消国有银行的贷款限额控制,各商业银行在推行资产负债比例管理和风险管理的基础上实行“计划指导,自求平衡,比例管理,间接调控”的新管理体制。20xx年,随着我国监管机制不断向新巴塞尔协议靠拢,各商业银行开始学习国外管理经验,开始引入缺口管理、持续期管理等模式,采用先进全面的资产负债管理手段提

3

升我国银行业经营水平和风险防范能力。

国内商业银行在资产负债领域近年来已经小有作为,例如回购业务迅速发展,普通债、次级债、混合债以及债券衍生品的推进,但在理论研究上国内还是较为落后,资产负债业务是商业银行生存和发展的基础,已经迫切需要对其进行系统性研究,并且服务于社会实践领域。

2、国外研究现状

近年来,美国等西方国家商业银行资产负债管理新的思想和理念不断涌现,量化工具和模型在国外银行和监管机构广泛适用;越来越多的国际大银行开始将资产负债管理的计量、评估、控制纳入资产负债管理决策模型体系,以协调不同经营风险,并进行前瞻性战略规划,实现模型科学性和实用性的统一。正如Gup and Brooks(1993)所指出,银行资产负债管理是为规避各种风险,增强流动性及提升银行市值,而基于法规、市场等约束下,考虑不同目标对银行资产负债所有项目的动态计划,其核心是银行重要的风险管理和战略财务规划工具。在这种背景下,基于情景分析和优化技术的资产负债管理决策模型由于其自身的诸多优点倍受学术界和实务届的广泛推崇。

(二)、发展趋势

与传统的商业银行资产负债管理相比较,现代管理不仅仅是防御手段,而是培育核心竞争力、创造竞争优势的有效手段。主要有以下发展趋势:

(1) 整合资产负债决策流程和工具手段,优化资产负债总量与结构;

(2) 全面推进资本管理体系建设,深化经济资本的多层面、多维度应用;

(3) 探索本外币资金的集约化经营,集中防范和控制市场风险;

(4) 优化内部资金转移价格传导机制,加快完善市场化产品定价管理基

础;

(5) 提高资产负债管理的电子化水平,培养资产负债管理复合型专业团

队。

三、毕业设计(论文)研究方案及工作计划(含工作重点与难点及拟采用的途径)

(一)毕业设计(论文)研究方案

第一章 绪论

第一节 研究背景与意义

第二节 文献综述

第二章 资产负债管理概述

第一节 资产负债管理理论的发展过程

第二节 资产负债管理的含义

第三节 资产负债管理的目标

4

第三章 我国商业银行资产负债管理状况

第一节 资产负债比例管理确立的过程

第二节 资产负债管理的现状和主要问题

3.2.1 资产负债管理外部环境的主要问题

3.2.2 资产负债管理内部实施的主要问题

第三节 资产负债管理问题的成因分析

第四章 我国商业银行资产负债管理的对策

第一节 完善商业银行资产负债管理内部制度建设

4.1.1设立资产负债比例管理指标

4.1.2引入资产负债管理技术方法

4.1.3建立高效的资产负债管理决策机构

4.1.4构建完善商业银行的定价机制

第二节 在资本规划的基础上加强风险资产管理

第三节 调整和优化资产负债结构

第四节 发展商业银行中间业务

第五节 利用金融衍生品交易加强资产负债管理能力

4.5.1我国金融衍生品市场的发展现状

4.5.2对我国商业银行资产负债管理的影响 结论与展望

致谢

参考文献

附录

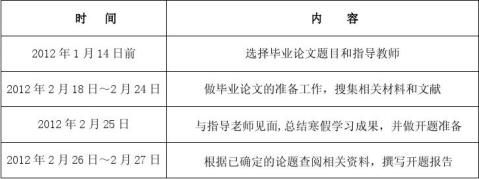

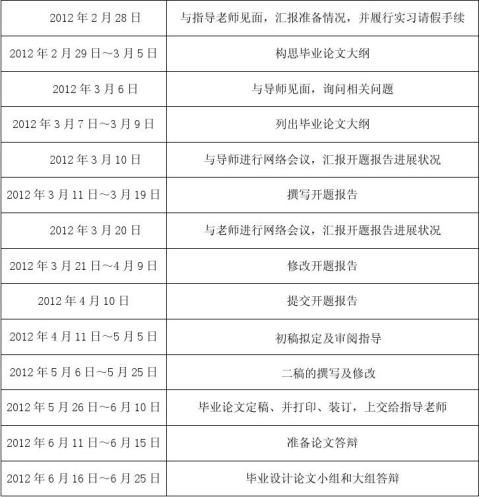

2. 工作计划

本课题研究工作计划如表1

5

3. 工作重点与难点

(1)工作重点:针对目前商业银行存在的问题提出解决措施从而提高商业

银行的核心竞争力。

(2)工作难点:提出相应的对策首先要适应商业银行运转的实际情况,然

而要使其真正发挥作用还要靠强有力的执行力。

途径: 1、查询文献资料; 2、搜集网络相关资料; 3、实际中的调查;

6

4、导师的指导。

四、主要参考文献(不少于10篇,期刊类文献不少于7篇,应有一定

数量的外文文献,至少附一篇引用的外文文献(3个页面以上)

及其译文)

[1] 王丽惠、刘莉:我国商业银行资产负债比例管理问题及对策[J],财政金融,20xx年,第246期:16-18

[2] 李华民:国有商业银行获利能力剖析[J],财经理论与实践,2001(5):109-111

[3] 彭建刚:现代商业银行资产负债管理研究[J].中国金融出版社, 2001

[4] 隆中佐:目前商业银行资产负债管理中存在的问题与对策[J],湖南商学院学报,20xx年3月,第9卷,第2期:101-104

[5] 梅卫红:加入WTO后我国商业银行资产负债管理的应对措施[J],新金融,20xx年第8期[6]:35-37

[7] Arzu Tektas,E,Nur Ozkan-Gunay;Gokhan Gunay.Asset and liability management

in financial crisis. The Journal of Risk Finance;2005;6,2:pg.135

[8]孟艳,金融危机冲击下资产负债管理的再审视[J] . 金融论坛,2010(2):170

[9]张金鳌,21世纪商业银行资产负债管理[M],北京,中国金融出版社:2002

[10]刘忠燕:商业银行经营管理学[M],中国金融出版社:20xx年

[11]熊继洲、楼铭铭:商业银行经营管理新编[M],复旦大学出版:20xx年

[12] DeYoung, Robert and Chiwon Yom“On the independenceof assets and liabilities: evidence from U.S. commercial banks,1990–2005”,Journal of Financial Stability,4 (2008) 275303.

[13] Modigliani,F.; Miller, M. (1958). “The Cost ofCapital,Corporation Finance and the Theory of Investment”. American Economic Review 48 (3): 261-297

[14]徐宝林,后危机时代的发展形势和中型银行的发展思路[J],当代银行家,第2期:23-24

[15] 何浩,2009,商业银行应对经济周期下行的国际经验及对中国的启示[J],

《国际金融研究》,第6期:46-47

[16].陈小宪,加速建立我国商业银行现代资产负债管理体系[J],证券时报,2002

(1):12-13

[17]许南.我国商业银行的市场风险及其防范[J]. 山东工商学院学报.2005(05):

43

[18] 赵燕. 转型期商业银行的资产负债管理[J]. 企业研究. 2009(12) :62-65

[19 黄璟. 探索建立现代商业银行资产负债管理体系[J]. 中国城乡金融报. 2004

(09):24

[20]Mulvey J,Shetty B. Financial planning via multi-stage stochastic

op-timization .Computers&Operations Research. 2004, (31) :1-20

[21]田灿明.中国商业银行投资理念研究[J].企业管理.2002(10):15-18

[22]鲁敏,徐聪聪.浅议我国商业银行中间业务的发展[J].商场现代化.20xx年第31期:26-28

[23]彭程;刘怡;杨红.金融衍生品交易对商业银行绩效的研究[J].江苏商论.2011 年第三期:35-36

7

外文文献原文

Title: Enterprise financing method: The general principles and EU law The third volume: funds, exit, takeover

Material Source: Women’s Consultation Briefing Paper

Author: Petri M?ntysaari

All firms lend and borrow. For example, the firm is a lender if it has a bank account in credit, and a borrower if its bank account is overdraw. The firm is a creditor if buyers pay for the firm’s Products after delivery and a debtor if it uses trade credit as a source of funding. Banks base their business on lending, borrowing, and buying and selling debt. Typically, most of the debt finance for small and medium-sized enterprises is provided by the banking sector. Firms might borrow to finance business expansion, meet day-to-day expense, or to ease short-term cash flow problems.

Advantages and disadvantages of debt. The use of the debt can bring the borrower many benefits: (a) In perfect capital markets, debt would be cheaper than shareholder’s capital, because debts must be repaid. (b) Debt is flexible. The firm can usually repay the debt when it no longer needs the funds. (c) The cost of the borrowing might be tax deductible. (d) Debt belongs to traditional corporate governance tools, because it gives the firm an incentive to be effective. In addition, debt doer not dilute existing share ownership. (e) In addition, return can be increased by gearing.

On the other hand, there may be some drawbacks: (a) Debt appears on the balance sheet, and too much debt will have an adverse effect on the firm’s debt-to-equity ratio. (b) A very high gearing increases the risk of business failure and can make it more difficult for the firm to survive in the long term. (c) Generally, a higher gearing and a higher debt-to-equity ratio can: signal an in crease in credit risk for banks, suppliers, and other providers of debt; lead to a lower credit rating, decrease the availability of debt; and increase its cost. (d) Although debt can be flexible, the formal and de facto powers of lenders may restrict managerial freedom and prevent the firm from taking important business decisions without creditor’s consent.

Types of debt. The firm can borrow money in various ways. (a) It can borrow

8

money from banks and other financial institutions under loan facilities. There are various kinds of loan facilities and loan instruments. The terms of bank lending are usually dictated by the bank. (b) Sometimes the firm can borrow from other non-financial firms. For example, the firm’s suppliers can extend credit in order to further of the borrowing. In this case, the firm may be able to negotiate the terms of the borrowing. (c) If the firm is large enough, it can also turn to the market and issue debt securities. In this case, the firm may be able to dictate its own terms subscribers of debt instruments find those instruments commercially attractive. (d) A debt instrument can be complemented by credit enhancements. (e) The firm can choose the seniority of the debt instruments that it issues by a combination of maturity (long or short), repayment schedule (regular repayments or bullet), and subordination (debt, collateral. Corporate structure ), and by using the equity technique in general.

Trade debts. Trade debts are an important source of funding. Trade debts were already discussed in the context of accounts receivable and accounts payable.

The firm usually does not pay interest on trade debts that it pays on time. In addition, the seller can sometimes grant a discount for prompt payment.

Trade debts can be a particularly important source of funding for powerful buyers that can force their suppliers to grant further discounts by claiming that the goods do not conform to the contract.

The role of trade debts depends on, among other things: the nature of the transaction; the country; and the parties. Sellers are more likely to extend credit if the transaction is a simple sale of goods transaction (say, oranges) and less likely to extend credit if the product is expensive and tailor-made for the buyer (e.g. a ship). The buyer’s country of origin plays a role. Because of a lower country risk and a different payment culture in Finland, a Finnish buyer is more likely to obtain credit than, say, a Nigerian buyer would be. The identity of the parties is important. For example, it is easier for the seller to extend credit in the context of an established business relationship, because the seller has already had an opportunity to verify such information about the quality of the customer’s payment behaviour that cannot be verified in advance.

Loan facilities. Commercial lending by banks can take various forms. The generic term “facility” is often used to describe them all and the terms loan facility and loan agreement ten to be interchangeable.

In principle, however, a distinction could be made between a loan facility

9

agreement and a loan agreement. The term facility reflects the fact that the lender makes a loan available to the borrower subject to certain conditions. The borrower might not have any obligation to borrow. Under a loan agreement, however, the borrower has agreed to borrow money, and is obliged to draw down.

Loan facilities can be with one bank or made available by a group of banks.

The most basic loan facility is the “term loan”. Term loans vary from the short term through the medium term. Term loan facilities provide that a bank is committed throughout a specified period to make advances upon request by the firm up to a maximum amount, with all the advances being repayable together. A term loan can have a fixed repayment schedule with a lump sum. Alternatively, the firm can borrow for a selection of periods, repay and borrow again. The facility may be available in a single currency or in a selection of currencies with an ability to switch from one to another.

The facility can be an advance facility or a bill or acceptance facility. An advance facility is a facility where the banks make cash advances to the borrower. A bill or acceptance facility involves the drawing of bills of exchange on the banks.

The firm can borrow either at interest or at a discount or premium.

Loan instruments. It can be seen that there is a wide range of loan instruments .For example, the firm can turn to a bank and agree on a facility. A medium-sized firm can raise short-term debt in the domestic money markets. A large firm can issue commercial bills or commercial paper. A large firm can also issue debt securities such as corporate bonds into the domestic primary market, or into the international market.

Loan instruments can differ in terms of seniority. The Economist described the wide range of loans instruments as follows: “With the new investors has come a bewildering variety of loans. Instead of a short chain – secured creditors, unsecured creditors and shareholders – now there are senior or first-lien creditors (who also have first dibs on a company’s assets), second-lien creditors (who also have claims over the assets of a company, but who get paid only after first-lien creditors),mezzanine creditors, senior subordinated debt holders and subordinated debt holders. At the bottom of this caste system, as before, are the shareholders, who get any leftovers”.

Nature of loan agreements. An intertemporal value transfer is characteristic of all loan transactions, and loan transactions are characterised by performances that are separated by a relatively long period of time.

10

The separation in time of the performances of the two parties influences both the underlying logic of a loan transaction and the dynamics of the negotiations between the borrower and the lender. First , the borrower might refuse to repay the loan when it falls due. The lender must therefore manage credit risk. Second , the lender counts on the borrower performing its obligations in a timely manner so that the lender will be able to repay its own obligations when they fall due. The lender will therefore have to manage refinancing risk.

IFRS. Accounting for loan relationships is important not only for lenders but also for debtors. Accounting standards set out when lenders may record loan assets at market value and when they must write down the asset. If the asset is written down, the lender will incur a loss. This will signal poor credit quality to other existing or potential lenders and, as the lender already has incurred a loss, make the lender less friendly.

The borrower will manage the risk exposure of lenders. For example, factors that signal a lower risk to lenders might include: a long history without defaults (this can signal that the borrower knows how to avoid credit default even in the future); unrestricted assignability (making exit easier); a large and diversified investor base (this can signal that the debt securities are liquid, that their market valuation is reliable, that there is easier exit, and that the risk of market collapse is lower); a dense distribution of maturities (this can signal that the borrower will be able to pay when securities fall due); and the existence of credit enhancements.

The borrower will also manage its own risk exposure. For the borrower, loan facility agreements can give rise to the same risks as contracts or funding contracts in general. In addition, some risks are characteristic of loan facility agreements in particular.

11

外文文献译文

标题:企业融资法:一般原则与欧盟法律 第三卷:资金,退出,收购 资料来源:斯普林格全文数据库 作者:Petri M?ntysaari 所有企业都贷款或借款。举个例子来说,如果企业拥有一个银行信用账户就可以作为债权人,公司银行账户透支那么就只能作为债务人。购买方购买企业商品后付款,这时企业是作为债权人,如果说企业是通过商业信用取得资金,此时企业就是债务人。银行的主要经营业务就是借贷和买卖债务。绝大多数中小企业的负债来源都是银行。企业借入资金,可以用于日常经营活动,或者用来解决短期流动资金不足的问题。

负债的优点和缺点。利用负债可以带来许多优势:(a) 在完善的资本市场中,负债筹资成本低于股本,因为负债是需要偿还的。(b)负债具有灵活性。企业可以在其不需要资金的时候再偿还债务。(c)负债经营可以减少税费。(d)负债是传统公司治理的一种工具,因为借入负债给公司带来了外在压力,起到了刺激公司经营的效果。此外,负债经营不会稀释股东的权益。(e)利用负债经营可以取得财务杠杆效应。

另一方面,负债也有许多的劣势:(a)负债作为资产负债表的一项内容列示,过多的负债会对公司的资本负债率产生不利的影响。(b)过多的负债会增加企业的风险并且会不利于企业的长期发展。(c)一般地,过高的负债额或者资本负债率会增加银行、供应商和其他提供借款的组织或者自然人风险,会导致企业信用等级的下降,会降低企业的再筹资能力,从而增加企业的成本。(d)尽管负债具有灵活性,事实上作为出借资金的一方会限制企业经营管理的自由并且在没有获得债权人同意的情况下会影响企业一些重要决策的作出。

负债的种类。企业可以通过多种渠道借入资金。(a)向银行和其他设有贷款业务的金融机构借款。现有各种各样的贷款融资方式和贷款工具,银行贷款的条件通常取决于银行。(b)有时候也可以向非金融机构借入资金。比如说,企业的供应商可以提供给企业一个信用额,在这种情况下,企业就可以对借款的条件进行谈判。(c)如果企业规模足够大,可以转向市场并且发行债券。如此一来,企业便可以自主地支配债务工具以吸引别人投资。(d)商业信用作为债务工具的补充。(e)企业可以根据一系列不同到期日的债务进行组合,制定还款计划(定期地还款或者重新借款)。

商业债务。商业债务是资金的一项重要来源。商业债务会在企业应收账款和应付账款的背景下进行讨论。

对于商业债务,企业通常不需要支付利息,一般考虑的只是时间的问题。此

12

外,卖家通常会在提示付款期内给予一个商业折扣。商业债务能够作为企业资金重要来源的一个原因在于对于强大的企业买主可以根据商品符合合同的不同情况要求供应商提供更多的折扣。

商业债务所扮演的角色主要取决于这些:交易的性质,不同的国家,不同的参与当事方。卖家通常喜好给一些简单的商品交易扩大信誉条件(比如说买卖橘子),而相较于比较大笔的交易或者是特定的交易,卖家就不太乐于扩大信誉条件(比如说买卖船只)。购买方所在的生产国也起着重要的作用。举例来说,由于芬兰处于较低的国家风险并拥有着不同的支付文化,一个来自芬兰的买家较一个来自尼日利亚的买家来说,更容易获得商业折扣上的优势。当事方的地位也是一个重要因素。如果一个企业的规模较大,信用情况较好,卖方就更加乐意给其扩大信誉条件,因为相对于较小规模的企业来说,卖方更能确保其到期收回款项的可能性。

设施贷款。商业贷款银行可以采取多种形式。通用术语“设施”可以用来描述所有情形,协议贷款和贷款协议通常是可以互相转换的。

然而在原则上,设施贷款与贷款协议还是有所区别的。术语“设施”反映的是这样一个事实,即贷款方提供贷款给借款人需要限定条件,借款人可能没有任何义务去借。而在贷款协议下,借款人主动提出借款并且有责任还款。

设施贷款可以通过一个银行或者是一组银行。

最基本的设施贷款是术语“放款”。放款是从中期贷款中分离出来的短期贷款行为,银行承诺为企业提供一个最大的贷款额度,除此之外,贷款还规定一个固定的期限。企业可以有选择性地选择不同到期日的贷款,之后还款,再进行筹资。

设施贷款可以是预支款、票据或者汇兑资金。预支款是指企业向银行提前透支的一笔款项。票据或者汇兑资金是指按照正常手续通过银行取得的资金。

企业可以通过利息借款也可以是以某一折扣借款或者是支付另外的手续费取得借款。

贷款契约。我们可以找到许多各种不同的贷款契约。比如说,企业可以转向银行并达成协议,一个中等规模的公司能在国内货币市场中提高短期债务,一家大公司可以签发商业票据;也可以发行债务证券(例如公司债券)进入国内主要市场或者到国际市场。

贷款契约就资历而言有很大的不同。经济学家对于广泛的贷款契约描述如下:随着新投资者的出现也形成了一系列让人眼花缭乱的贷款。然而,有所区别的是,现在拥有第一优先权的是具有担保债权的债权人,而不是无担保的债权人和股东。拥有第二优先权的是对企业的资产有要求全但是次于第一优先权的债权

13

人。另外还有夹层债权人、主要附属债务持有人和附属债务持有人。作为股东,只有最后的求偿权。

自然的贷款契约。一个跨价值观迁移的特点是全部贷款交易,它已经从履行交易中分离出来了很长时间。

所有权与经营权的分离同样地影响了交易中债权人与债务人。第一,债务人可能会在借款到期日拒绝付款,因此债权人就必须要承担债务风险。第二,债权人需要监督债务人经营以到期可以要求债务人及时履行还债义务收回资金。债务人同样需要管理风险。

国际财务报告准则的限制。会计准则对借款人和贷款人两者的借贷关系中的任何一方都很重要。债权人借出资产就可能需要计算市场中存在的资产并且必须将资产记录下来,这就需要从会计准则出发。一旦资产被记录下来,债权人就可能会产生损失。这种情况就会使得一些潜在的债权人或者已经遭受损失的企业不愿意借资金给那些信用等级差的企业。

债务人借款可能会对债权人产生风险。举例来说,债务人风险较低的情况包括:企业历史悠久并且没有违约记录(这表明债务人知道在未来如何经营避免到期不能偿还债务),存在不受限制的可转让性财产(使还债更加容易),拥有比较大的投资项目(这样表明债务资金的流动性较强,债务人市场活跃,相对于债权人来说,市场风险较小),成熟的摊销方法(表明债务人有能力在到期日还款),规范的信用改进措施。

另外,债务人需要控制自我风险。就债务人而言,一般情况下融资协议签订后都会产生还款的风险,在特定情况下还可能会产生许多特殊的融资协议风险。

14

15