A financial analysis report for Tricol plc Outcome 3and4

Class;10E6 Name:Ma boda SCN:125099297 Candidate Num:22

Introduction

To operate better in financial aspect, the management of Tricol plc asked me to analyze their financial condition then make recommendations for them.

Findings

Part A

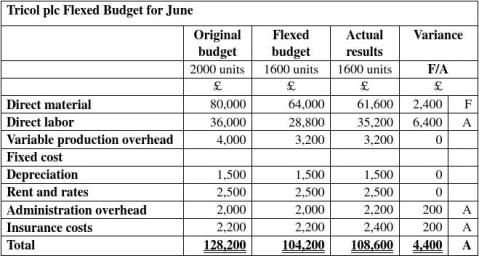

(ⅰ) Flex budget in line with actual activity

(ⅱ) Variances calculation

(Standard units of actual production*standard price) -(actual quantity*actual price) (4 kg*1,600*£10) -£61,600 =£ 2,400 (F) Rate of significance: (3.75%) Standard price*(standard units of actual production - actual quantity)

£ 10*[ (4kgⅹ1,600) -5,600kg]= £8,000 (F)

Rate of significance (12.5%)

Actual quantity * (standard price - actual price)

5,600kg*[£ 10 -(£61,600/ 5,600kg) ]= £ (5,600) (A)

Rate of significance: (8.75%)

(Standard hours of actual production*standard rate ph) - (actual hours*actual rate ph)

[ (2hrs*1,600) *£9]-£35,200=£(6,400) (A)

Rate of significance: (22.22%)

Standard rate ph* (standard hours of actual production - actual hours)

£9*(2hrs*1,600-3,520hrs)=(2,880) (A)

Rate of significance: (10%)

Actual hours*(standard rate ph – actual rate ph)

3,520hrs*(£9*-£35,200/3,520hrs)= £(3,520) (A)

Rate of significance: (12.22%)

Total standard overhead for actual production - total actual overheads

(£18,000/12+£2,500+£2,200+£2,000)- (£1,500+£2,500+£2,200+£2,400)=£(400) (A)

Rate of significance: (3.5%)

(ⅲ) Report about variances

? Direct material variance

The direct material total variance can be analyzed in two aspects which are direct material volume and direct material price.

For volume side, as calculated above, the budget volume is 6400kg; the actual volume is 5600kg. So there is 800kg variance which is favorable and each unit variance is 0.5kg. The likely reason causing the variance comes from three aspects. First of all, the company upgraded the production machinery recently, and new machine may use materials efficiently, so it reduced the waste of materials. Secondly, the company switched suppliers and using higher-grade materials can decrease waste of materials too. Finally, the company has concluded a higher-than-expected wage settlement for production operatives, which will maintain employees with higher skills as well as

decrease turnover of employees, and it also can increase efficiency in using materials.

For price aspect, the budget price is £10 per kg, and the actual price is £11per kg, it is adverse that one pound over the budget price. The company switching suppliers may cause the increase of negotiation cost. There may be a long-term relationship between Tricol plc and its old suppliers, so the suppliers may take lots of discounts to the firm. After changing suppliers, the discount may disappear. Furthermore, higher grade materials increased unit price.

Overall, the total material variance is favorable. £8,000 -£5,600=£2,400.

? Direct labour variance

The direct labour total variance is composed of direct labour efficiency variance and direct labour rate variance.

The budget direct labour hours are 3,200hrs and the actual labour hours are 3,520 hrs. There are more 320hrs needed than the budget, and each unit is 0.2hrs, which it is

obviously adverse. The company upgrading the production machinery may need time for employees to adopt it. Also, employees need training time. The rebuild process of machinery consumed time too. In a word, the chargeable hours have increased.

The budget direct laour hours rate is £9 per hour, the actual hours rate is £10 per hour. It is adverse that one pound higher than budgeted. It is possible caused by both internal and external factors. Higher-than-expected wage settlement may be internal reason for the variance, and new machinery may be needed to recruit new employees to operate the machinery, which also can increase the expense. For external factors, the changing of labour market may increase labour cost; the government legislation also can increase the labour cost, for example minimum pay.

Both direct labour efficiency and direct labour rate variances are adverse, so the direct labour total variance is adverse.

? Overhead variance

As calculated above, total overhead variance is caused by administration and

insurance. Each factor has £200 variance, so the total overhead variance is £400 and it is adverse. During the process of changing supplier, the company needed more expense on public relationship or negotiation, in addition, in order to maintain the new machinery, administration cost will be increased too. For insurance aside, the improvement of machinery will need more insurance fees to cover, which also contributes to the increase of insurance fee of new employees.

Part B

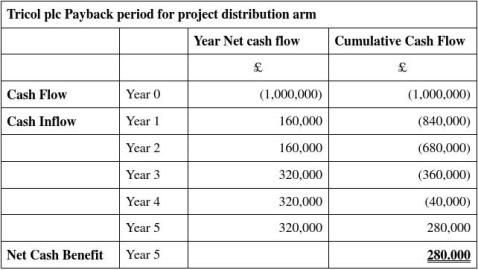

? Selection and application of two investment appraisal techniques

As the company is keen to recoup the cost of the investment within five years, I will choose Payback period and Net Present Value to help me complete the appraisal.

In order to fulfill the appraisal easily, there are some assumptions listed below should be considered before the appraisal. ⑴ All revenue and inflow are assumed cash flow ⑵ All investment cost incurred in year 0 ⑶ No uncertainty is considered

⑷ Do not consider inflation and taxation ⑸ Market rate of return is expected rate of return ⑹ Rate of return is varying along with time

Note: req uire 40,000/320,000 in year 5= 1/8*year=1.5 moths Payback=4 years 1.5 moths

? Recommendation about investment

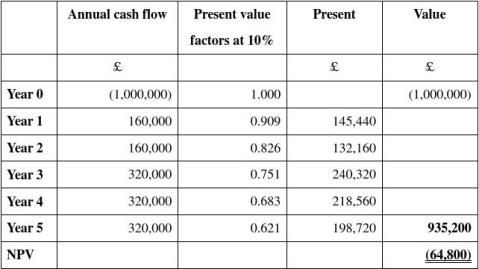

According to Payback Period analysis, the investment cost can be recouped in year 4 and 1.5 moths. In other words, the period is under company’s expectation. The project can be executed. However, according to Net Present Value analysis, in terms of present value, within five years, what the NPV will bring net result is net cash loss but not net cash surplus. In general, the company should consider time value and other factors, so the project should not be executed.

? Factors impact on the investment should be considered

Various factors will impact on result of investment. I will outline factors should be considered when the management reviewing my recommendation in financial and non-financial factors.

? Financial factor

As distribution arm is financial long-term beneficial project, it can be used in

long-term period and bring benefits continuous. The investment cost is £1,000,000, which can be considered a large investment. So it more likely needs long period

payback period. The management should focus on longer cash flows for longer period of future. On the other hand, Net Present Value in year five is (28,000) only take 2.8% percents of the investment cost, it is more likely surplus in year six. Another financial factor is source of million pounds. If it is internal source, the management mainly concentrate on opportunities cost. If it is cost of capital or cost of capital taking much weight of the source, the management must pay cost of the source firstly, the marketing rate of return likely low for the company, in addition, the management should use higher discounted cash flow.

? Non-financial factor

The investment must be consistence with company’s strategic plan. As Tricol is a plc, it must take social responsibility such as obeying government policy, minimizing impact on environment and minimizing impact on natives.

Conclusion

For real competition is more complex and fierce, in order to make accurate decisions, management should consider more factors during the decision-making; furthermore, the management should use more tools to help them such as IRR, DCF.